ZIMBABWE is experiencing a sense of macroeconomic stability so far in the second half of 2023 (2HY23). While authorities expect this stability to hold throughout the 2HY23 and beyond as illustrated in the 2024 budget strategy paper (BSP), many lingering risks are threatening the stability of the economy.

In this column, therefore, I analyse the 2024 BSP to identify probable economic outlook risks and proffer some policy alternatives that can help minimise the impact of these risks.

2024 fiscal policy thrust

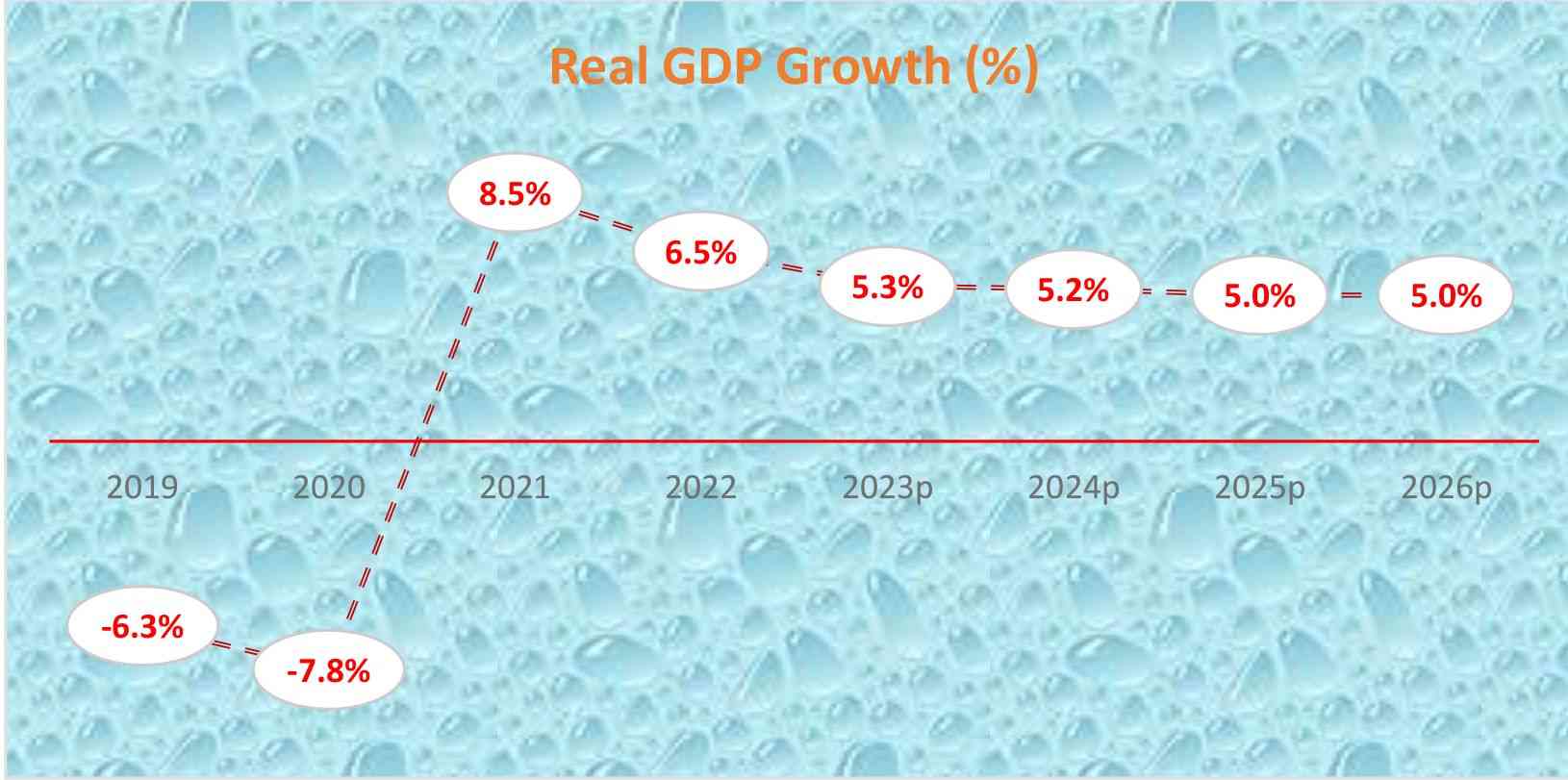

The latest 2024 Budget Strategy Paper (BSP) is projecting a GDP growth rate of 5,2% next year. Treasury posits that this growth will be anchored on sustainable budget deficits (less than 3% of GDP) to contain Zimbabwean dollar (ZWL) depreciation and price inflation.

Also, the Treasury promised to follow a prudent approach to fiscal management (cash budgeting, raising additional tax revenue, containing spending and efficient resource use) in 2024.

More so, fiscal authorities promised to pursue a robust reform agenda (arrears clearance, debt relief and resolution strategy, redressing high input costs and low productivity, and reforming public entities). While the foregoing fiscal policy thrust for 2024 is highly commendable.

Treasury must ensure that it also meets some key spending benchmarks.

Generally, domestic, regional, and global budget spending benchmarks, such as the 20% Dakar Declaration on education and the 15% Abuja Declaration on healthcare are established to function as indispensable tools for addressing the transparency and accountability deficit associated with long-term targets.

- 2024 budget strategy paper: Zim’s future looks bleak

- Fiscal overruns haunt Zim

- Qualitative contradictories of Zimbabwe 2024 budget

- Village Rhapsody: Why Zimbabwe is struggling to fix its currency conundrum

Keep Reading

As such, the 2024 budget must endeavour to adhere to these benchmarks when appropriating budget votes if Zimbabwe is to attain economic growth and development that is stable, inclusive, and sustainable.

This is the thrust of the 10-year National Development Strategy (NDS) (2021-2030) of leaving no one and no place behind in Zimbabwe’s quest for attaining an upper-middle income status by 2030.

2024 revenue strategies

The Treasury projects that it will collect about 19,2% of the projected nominal GDP (ZW$159,7 trillion) as tax revenues in 2024. This will be underpinned by tax administration initiatives to enhance tax enforcement and compliance and adoption of technology. It is stated that the tax base will be expanded through an embrace of emerging industries and the capture of the digital marketplace.

Authorities will endeavour to review concessions and contracts undermining revenue collection as well as adjust fees, charges and levies in line with the cost recovery principle. In addition, revenue leakages from corrupt activities will also be curbed.

To me, these proposed measures are welcome as long as they will safeguard both vertical and horizontal tax equity and lessen the tax burden on economic agents particularly poor households.

2024 expenditure strategies

Treasury envisages a budget ceiling totaling ZW$33,1 trillion in 2024, up 29,3% from a ceiling of ZW$25,6 trillion now projected for 2023. This expenditure ceiling will be limited to available resources and the fiscal deficit will not exceed 3% of GDP in line with the NDS1 target.

According to the Treasury, the size of the 2024 wage bill will depend on the extent of wage compression, gaps in service delivery, and skills flight. Again, there will be retention schemes for critical staff, performance contracts, strengthening of value for money (VFM) audits, and plugging out procurement loopholes.

However, just as is the case with the 2023 budget, the 2024 budget will likely exceed official projections. The 2023 budget has ballooned five times to ZW$25,6 trillion from ZW$4,5 trillion that was initially anticipated.

Largely driving this staggering growth of nominal expenditures is hyperinflation experienced in the 1HY23 as the local currency lost at least 80% of its value against the USD. Since 2019, these exchange rate fluctuations and resultant galloping inflation have greatly affected approved ZWL-denominated national budgets leading to unauthorised excess expenditures.

So, going forward, robust expenditure containment measures will require adequate political will to swiftly institute reform matrices that were agreed with creditors: governance, land tenure, and economic reforms.

These reforms are the only durable way to subdue recurring inflationary pressures, mobilise domestic resources, reduce waste in government, increase market competition and innovation, and improve productive efficiency (producing goods at the lowest cost) and allocative efficiency (optimal distribution of goods and services, taking into account consumer’s preferences) in the market.

2024 macro-economic outlook

The severe macroeconomic fluctuations witnessed in the first half of 2023 (1HY23) compelled authorities to institute a plethora of policy measures to tame instability.

Largely due to these policy actions, ZWL depreciation, and price growth moderated significantly from July 2023 through August.

Buoyed by this sense of stability, authorities have revised the 2023 national output (GDP) growth projections to 5,3%, up from the initial projection of 3,8%.

According to the Treasury, the revision of the 2023 GDP growth projection is supported by a relatively better 2022/23 agriculture season, ongoing public infrastructure projects, and relatively favorable global mineral commodity prices.

High global mineral prices are being sustained by recurring supply uncertainties posed by the Russia-Ukraine war as well as a global seismic shift toward green energy.

Furthermore, so far in the 2HY23, the nation is enjoying improved domestic electricity production largely emanating from recently commissioned 2 new thermal units with a combined installed capacity of 600MW.

In addition, ZWL depreciation and inflation which are trending southwards so far in 2HY23 can exert some positive spillover effects on the economy by boosting consumer demand, increasing market confidence, encouraging savings and investment, and maintaining international competitiveness.

However, Zimbabwe faces various risks that may undermine the projected 2024 GDP growth.

These risks include the likely persistence of exchange rate and commodity price volatilities, which will adversely affect revenue collection, service delivery, and debt servicing costs.

There are also revenue risks that may emanate from reduced tax compliance, rampant corruption and impunity, and rising economic dollarisation which breeds informality and tax evasion.

More so, a disputed election is compromising the legitimacy of the declared winner.

This may likely have a negative bearing on international relations and cooperation, foreign direct investment (FDI), official development assistance, and structured dialogue with creditors.

Also, electoral contestations may lead to deep societal polarisation, politically motivated violence and conflict, disruptive partisanship, elevated white-collar corruption in government, poor service delivery, plunder of natural resources, and capital flight, among others.

Even though electricity production has improved in the 2HY23 as alluded to earlier, hydro output from Kariba Dam is facing serious threats from dwindling dam water levels while frequent breakdowns of aging Hwange thermal (Units 1 to 6) will keep constraining thermal output.

If this holds, minimal power rationing schedules being currently experienced across the nation will likely worsen and cripple economic activity unless there are significant incentives to lure private sector investments into the energy sector.

Furthermore, there is a high likelihood of expenditure risks emanating from elevated interest rates, structural budget rigidity, and limited fiscal space.

Again, for an agro-based economy that is too dependent on rainfall like Zimbabwe, the latest projections of El Nino weather conditions (below-average rainfall and above-average temperatures) for the upcoming 2023/24 summer cropping season will likely spell huge disaster – crop failure, high food prices, and food insecurity.

As such, there are high chances of above-average fiscal spending in the 2HY23 and beyond as the government is expected to cushion the economy and its citizens from a likely devastating drought.

Elevated fiscal spending increases ZWL liquidity in the market thereby destabilising the ZWL and market prices.

Last but not least, negative spillover effects emanating from deteriorating geopolitical tensions fuelled by the Russia-Ukraine war such as higher input prices and dislocation and disruption of global supply chains will constrain economic activity.

Therefore, mitigating these 2024 budget risks will require political dispute resolution, strengthening of existing legal and regulatory frameworks, adoption of accruals accounting, capacitating oversight and accountability institutions, embracing domestic resource mobilization, diversifying the economy (value addition and beneficiation), providing affordable and accessible public services, engaging and re- engaging with the global community, and implementing reforms to strengthen democracy, improve government efficiency, and subdue pricing distortions.

- Sibanda is an economist. He is a research associate with Zimcodd. He is a staunch advocate for inclusive and sustainable development. He writes in his personal capacity.