Victor Bhoroma THE Reserve Bank of Zimbabwe (RBZ)has introduced a new ZW$100 note,which will be the highest denomination in the local market. Using the government pegged foreign exchange auction rate, the bill is worth US$0.68.

However, if the benchmark parallel market exchange rate is used the value of bill falls to US$0,30, which means that consumers need three such notes to buy a loaf of bread.

The delayed introduction of the ZW$100 bill renders all the notes below ZW$50 valueless; with the ZW$20 (US$0.05) only sparred for a few weeks to allow traders some coinsfor change in small transactions.

Since 2019, the central bank has used millions worth of real money to print and ship Zimbabwean dollar notes and coins from abroad into the economy.

The apex bank will soon be forced to decommission most of thosenotes and coins below the recently introduced ZW$50 as inflation accelerates again.

History of money printing Annual inflation for March 2022 advanced to 73%, up from 61% as of the beginning of the year. The central bank set a 25-35% annual inflation target for end of 2022.

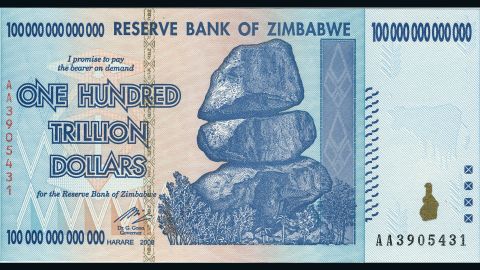

This is already out of reach with annual inflation expected to creep back to triple digit figures and end the year at about 120%.Zimbabwe has already had to grapple with record-breaking hyperinflation of November 2008 when month-on-month inflation reached 79,6 billion percent per month, with annual inflation reaching an astounding 89,7 sextillion in December 2008.

The Inflation run only stopped after the country adopted the US dollar in April 2009 to save the economy from total collapse. However, in November 2015, a local currency (bond notes) was introduced in the market.

- Chamisa under fire over US$120K donation

- Mavhunga puts DeMbare into Chibuku quarterfinals

- Pension funds bet on Cabora Bassa oilfields

- Councils defy govt fire tender directive

Keep Reading

The bond notes seemed to maintain value on paper for three years. However, the economy was experiencing high levels of foreign currency withdrawal and externalisation. Bond notes completely lost value after the printing run started again in October 2018, taking annual inflation from 5% in October 2018 to double digit figures of 42% in December 2018.

After the formal re-introduction of the Zimbabwean dollar as RTGS in February 2019, inflation increased from 57% in January 2019 to 838% in July 2020.

Throughout history, the Zimbabwean economy has collapsed and lost billions in savings and investment because of money printing with the War Veterans gratuity payments wiping off 72% off the Zimbabwean dollar value in one day on December 14, 1997 (Black Friday).

The DRC war funding from 1998 to 2003 had double theimpact on the economy. Therefore, the major cause of inflation in Zimbabwe is money supply growth(in physical notes or electronic money) by the central bank to fund excessive government expenditure or monetise budget deficits.

Lack of confidence in the domestic currency happensbecause of pure currency mismanagement and inconsistent monetary policies. Other causes such as debt, declining production, drop in exports, exchange controls and geopolitical pressures are secondary (peripheral in certain instances).

Central bank mandate As is the case in the world, the main function of the central bank, according to the RBZ Act, Chapter 22.15 are to formulate and implement monetary policy directed at ensuring low and stable inflation levels.

Additionally, the bank is mandated with maintaining a stable banking system through bank supervision and lender of last resort policies, issuanceof bank notes and coins and management of the country’s gold and foreign exchange assets to support the domestic currency. However, the contentious function of the central bank relates to its role of acting as a banker and fiscal agent of the state.

Section 8 of the RBZ Act points that nothing shall prevent the state from carrying on transactions in such manner as the state may require and, if so, requested by the state through the minister in writing, the Bank shall make the necessary arrangements to this end.

It is this function that has led to conflation between monetary policy and government policy to fund unbudgeted expenditure or political programmes.

Central bank quasi fiscal activities Between 2005 and 2008, the Zimbabwean central bank carried out various quasi fiscal operations that were key drivers of hyperinflation in the economy.

These included the 2005 Agricultural Sector Enhancement Productivity Facility (ASPEF), Operation Maguta, Parastatals and Local Authorities Reorientation Programme (PLARP) and the Basic Commodities Supply Side Intervention (Baccossi).

Since the RBZ Debt Assumption of 2015, the bank has been running with several quasi-fiscal activities, such as, supporting small scale gold and tobacco production, funding consumption subsidies (for commodities such as fuel, cooking oil, wheat, soya, and others), boosting tourism, funding agricultural inputs, cross border trade and export incentive schemes, among others, while crowding out the country’s financial institutions such as commercial and merchant banks.

These quasi-fiscal activities have directly contributed to inflation growth and have various rent-seeking loopholes that nurture corruption to this day.

Currently, the central bank has taken the role of allocating foreign currency in the economy via the auction allocation system, even sinking to the level of incurring billions foreign debt to support the prevailing exchange control model. This would not be necessary if the foreign exchange market was liberal.

Lessons from Gambia Gambia has an economy of about US$1,8 billion (12 times smaller than Zimbabwe), export receipts of US$360 million(Compared to Zimbabwe’s exports of US$6,3 billion) and imports of US$1,7 billion in 2021.

In 2020, Gambia had foreign currency reserves of US$258 million while Zimbabwe had US$33,5 million, according to World Bank data. The value of the Gambian Dalasi has maintained value at US$1: GD50.23in January 2019 to the US$1: GD53.35 as of April 12, 2022 (over three years).

Money supply in Gambia grew by 22,5% in 2020, while in Zimbabwe it grew by 486% in the same year. The country operates a managed floating exchange rate and annual inflation averages 7,7% since 2019.

The Consumer Price Index (CPI) in Gambia increased to 116,43 points in February from 115,98 points in January of 2022, while CPI in Zimbabwe increased to 4766,10 points in March from 4483,10 points in February of 2022.

The major reasons for economic stability in the Gambia are that the Central bank of Gambia sticks to its core mandate of managing inflation, building reserves and printing money in tandem with economic growth without engaging in quasi fiscal activities.

Currency stability in other countries The bank of England (where most central banks in the world borrow their model from) is owned by the government of the United Kingdom since its nationalization in 1946.

In May 1997, the Bank of England (BoE) was given operational independence over monetary policy to curtail political influence from government to implement policies that favour short term political objectives.

Most central banks in Africa are wholly owned by the state, including current flag-bearers in economic transparency such as Mauritius, Tunisia, Morocco, Botswana, Rwanda, and Ghana.

However, the level of inflation and economic stability in those countries is directly correlated to central bank transparency and monetary policy independence.

As a result, ownership of the central bank is the same, what distinguishes various economies is the level of transparency and institutional mechanisms that bring good governance, transparency, and public confidence.

Zimbabwe’s central has over the years been involved in funding public sector programmes that are not part of its mandate, thereby, shredding the whole economy.

Inflation is largely a function of money supply in the local economy, not the supposed fear of free market policies or other exogenous factors. Provided money supply growth is aligned to economic growth and kept low in an inflation targeting framework, foreign exchange prices will stabilise since the source of money largely finite.

Foreign exchange stability and consistency are more important than the exchange values. The challenge with the central bank is that it cannot let foreign exchange prices be market determined because it needs to print money while getting foreign currency at sub-economic prices from exporters.

Critically institutional reforms that bring monetary policy independence are long overdue at the RBZto separate politics and monetary policy. Inflation continues to wreck the local economy, subdue investment, dismantle savings and above all subdue millions of Zimbabweans to abject poverty.

Parliament needs to be empowered to hold the central bank to account and enforce transparency in the interest of public good and economic stability.

Economic stability can only be sustainable through instilling market confidence in monetary policy, implementing free market policies on exchange control and abiding to full disclosure on central bank debt and its utilisation.

It is government’s prerogative to chat policies that shape public expenditure towards political and economic objectives, but it is economically immoral to resort to printing money for short term political goals. Monetary policy dictates the pace of economic growth and livelihoods in any nation, as such it should not be left to the executive arm of the government to control it.

In the end, the buck stops on political will to institute reforms at the central bank and stabilise the local currency as is the case in other stable African economies.

- Bhoroma is an economic analyst. He holds an MBA from the University of Zimbabwe (UZ). — [email protected] or Twitter @VictorBhoroma1.