RESPECT GWENZI A PLUNGE of 3,07% in the value of the local unit, the Zimbabwean dollar (Zimdollar), was in line with the prior week loss. It is ranks as the third worst performance since the beginning of the year.

Since January, the auction market has completed a total of 11 sessions and the average weekly loss over the period came in at 2,5%.

Cumulatively the Zimdollar has lost 27,4% since the beginning of the year, which is almost close to what the embattled currency over the whole of 2021.

For the 12 months period to December 2021, the Zimdollar lost 28,8%, which means the full year loss from last year will be surpassed by the first week of April.

This is worrying and alarming at the same time, given the implication of currency stability on the general economic stability of Zimbabwe. The import of the weak currency performance is that it reflects on weak economic fundamentals, monetary expansion and high inflation outlook.

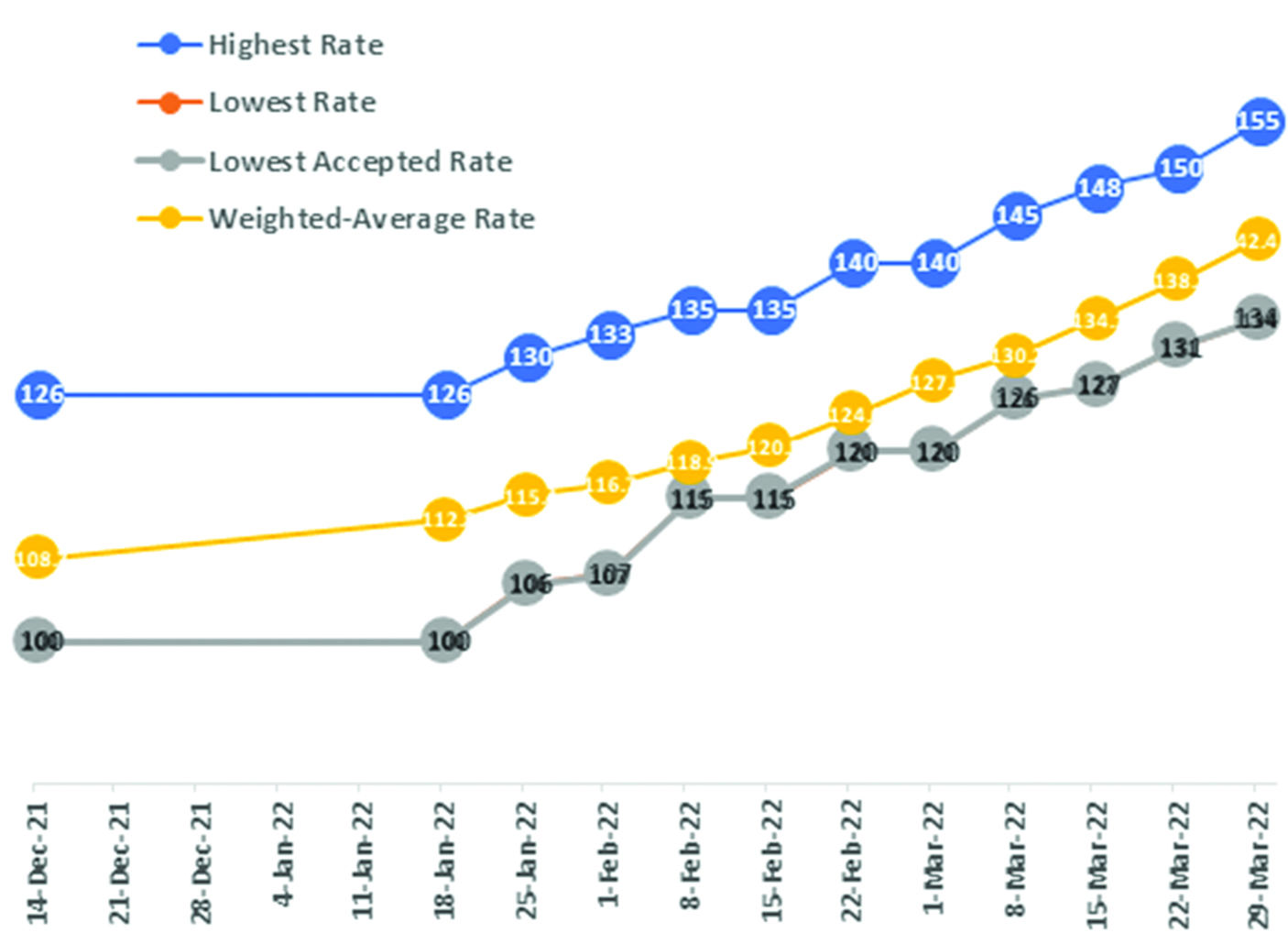

The top bid level moved up to 155 from 150 last week. The top bid has moved up in each respective session since the beginning of the year, except in only one.

Cumulatively the top bid has moved up by 29 points year-to-date. The lower and lower accepted bid has moved in synch since the beginning of the year and this week moved up by three points to 134.

The spread between the top and lower bid came in at 21 points, which was unchanged from last week. The interplay between the lower and upper bid has failed to give us an indication on future market direction.

- Chamisa under fire over US$120K donation

- Mavhunga puts DeMbare into Chibuku quarterfinals

- Pension funds bet on Cabora Bassa oilfields

- Councils defy govt fire tender directive

Keep Reading

However, the unison movement upwards shows that the outlook is likely to remain pessimistic as the exchange tumbles.

The effect of the big jumps in the exchange rate is that inflation will tend to rise at faster rates. We now anticipate an inflation outturn of close to 100% by April based on the sunk movements in the exchange rate.

A 30% plunge in the formal exchange rate, should culminate in at least a 20%+ movement in inflation. Much of the impact on inflation will emanate from the movement in the parallel exchange rate.

It will increasingly become very difficult to control inflation levels above the 100% mark, as history has shown. Although government has declared successive surpluses, it has been more aggressive on the Treasury Bills (TBs) market and this is reflecting in the growth in broad money supply.

Borrowings from the open market are being used to siphon excess liquidity from the market as well as to finance government programmes, such as the ongoing infrastructure projects.

The projects are massive and contractors are getting preferential exchange rate on their invoices.

So while government has done much to maintain a stable reserve money level, its appetite for debt mainly via TBs and bonds has been out of order, reminiscent of yester year behaviour.

Latest data from the Reserve Bank of Zimbabwe shows that Broad Money Supply (M3) swelled by 113% between January 2021 and January 2022.

Against this, TBs and bonds held by commercial banks and by other depository corporations totalled ZW$78,9 billion as at January 2022 from ZW$18,6 billion as at January 2021, which is a growth of 324%.

This debt measured in US dollars using the average exchange rate over the period comes in at US$650 million. This is about 16% of the national budget for the respective year of 2022.

The impact of such a huge debt accumulation is the growth in money supply of the local currency. This is the reason why the exchange rate is crushing and nearing about US$1:ZW$300 on the parallel market.

This brings us to another dimension of the currency crisis. The Zimdollar is trading at almost twice the formal rate, on the parallel market.

This is largely due to the manipulation of the formal rate by the RBZ. How this is done is well documented in our previous publications.

The central bank manages liquidity through a weekly auction, instead of a decentralised minute trading at authorised financial institutions.

Liquidity is managed through a compulsory surrender requirement targeting exporters, making the central bank the largest forex supplier.

The trading system punishes top bids as lower bids are satisfied. The RBZ can tactically use its liquidity to satisfy very low bids and leave the rest for other players, thus dragging the weighted average exchange rate. This would go on to inform all interbank trades for week. This is an imperfect forex management system, even as the RBZ posits both as a player and a referee.

This conflict gives it room to declare funds, which it does not currently have, creating serious backlogs, speculation and lack of confidence in the system.

- Gwenzi is a financial analyst and MD of Equity Axis, a financial media firm offering business intelligence, economic and equity research. — [email protected]