RESPECT GWENZI THIS week the Zimbabwean dollar (Zimdollar) dropped by yet another noteworthy margin against the greenback, on the auction market.

The Zimdollar has lost value in each of the 10 trading weeks since the beginning of the year and the cumulative total loss over the period is now marginally shy of last year’s full year loss level.

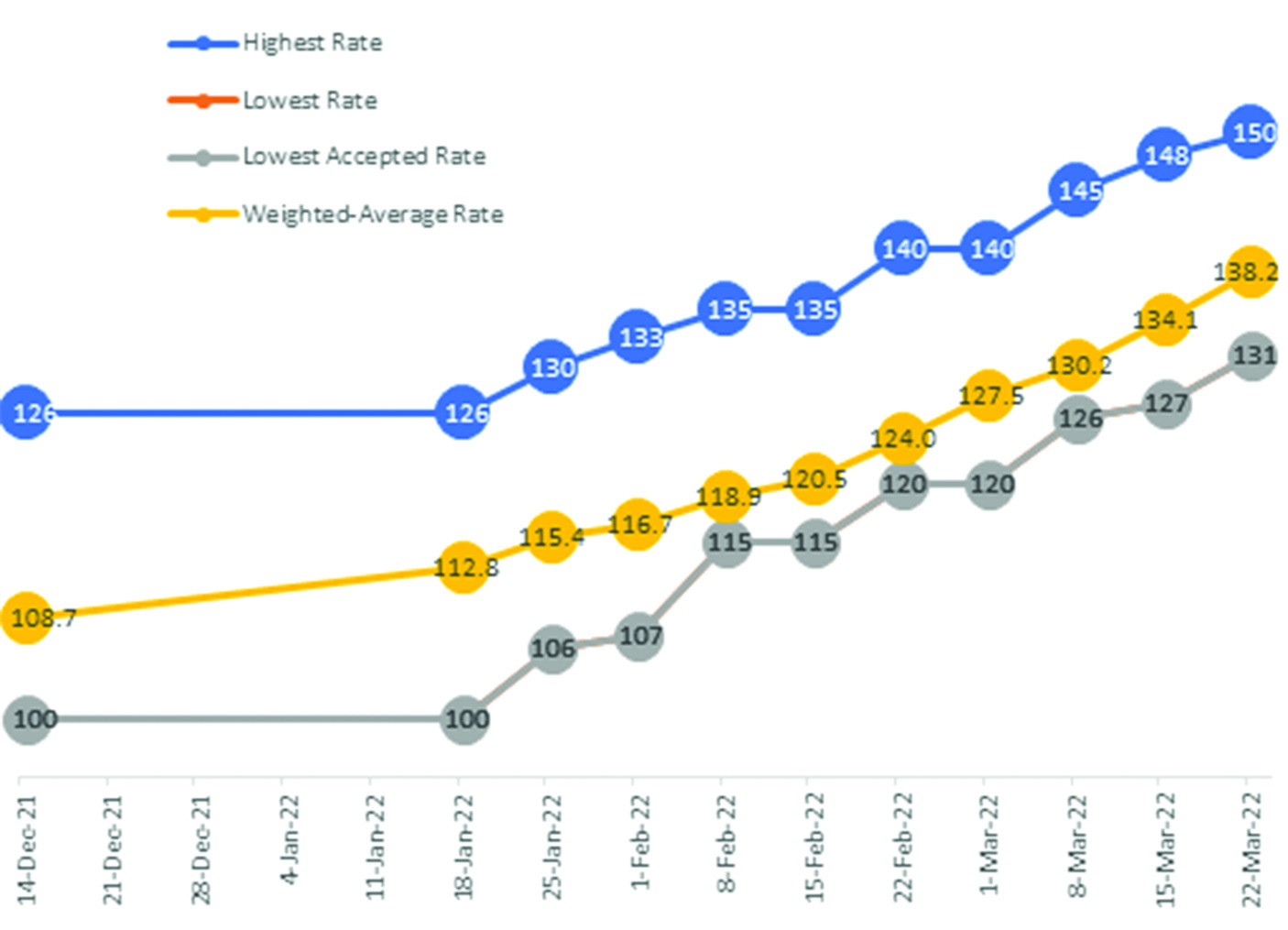

A loss of 3% incurred in this week’s session is the second worst since the beginning of the year as shown in the chart below.

On average, the Zimdollar has been losing 2,4% a week since the beginning of the year and in its worst performance, which was in the first week of the year, it lost a whopping 3,7%.

The cumulative loss year to date moved up to -23,7% after this week’s loss. This is only 4% shy of reaching the full year loss of 28% incurred for the whole year in 2020.

This is unprecedented and unexpected at least from the official viewpoint carried by the Reserve Bank of Zimbabwe. The bank is running with a narrative of stability, which is not at all true.

The bank misconstrues a slow and gradual increase in prices over the last two months as a reflection of currency induced stability. We will explore that misconception later in this review.

The top bid level moved up to 150 from 148 last week. The top bid has moved up in each respective session since the beginning of the year, except in only one.

- Chamisa under fire over US$120K donation

- Mavhunga puts DeMbare into Chibuku quarterfinals

- Pension funds bet on Cabora Bassa oilfields

- Councils defy govt fire tender directive

Keep Reading

Cumulatively the top bid has moved up by 24 points year to date. The lower and lower accepted bid has moved in synch since the beginning of the year and this week moved up by three points to 131.

The spread between the top and lower bid came in at 19 points, which was unchanged from last week. The interplay between the lower and upper bid has failed to give us an indication on market direction.

However, the unison movement upwards reflects that the outlook is likely to remain pessimistic as the exchange tumbles

The movement in the exchange rate between the parallel and formal market has not been congruent. The parallel market moved by a higher margin between January and February while the official market lagged, mostly because of the annual break.

Over the annual break between December 2021 and January 2022, the parallel exchange rate shed over 30% taking the premium to levels close to 100%.

The lag gave an impression of exchange rate stability, but the reality was a widening gap.

What we are seeing presently is the catching up of the formal rate to the parallel market. At premium levels of about 90% we expect that the auction market will continue to record weekly losses of above 2%, until the gap close nearer to 50%.

This projection is premised on the performance of the currency in past period, given the varying premiums. With the official exchange rate moving up at quicker paces, we expect the cost of utilities to rise in tandem among other services offered by the government, resulting in higher inflation.

In terms of the exchange rate outlook, we are of the view that for the rest of the first half period, the gap between the two rates will maintain margins of above 50%, hence sustaining the downward momentum in the official.

The biggest driver of currency weakness is the growing money supply levels at M3, swelling government expenditure outside of the budget, speculation and a lower-than-expected growth rate.

- Gwenzi is a financial analyst and MD of Equity Axis, a financial media firm offering business intelligence, economic and equity research. — [email protected]