‘I’ll crush the black market’ … RBZ boss vows to smash US$2,5bn menace, bring stability

Local News

By Shame Makoshori | Apr. 12, 2024

Zimbabwe’s black market has so much power and influence to determine the exchange rate, which formal businesses have been whipped into accepting.

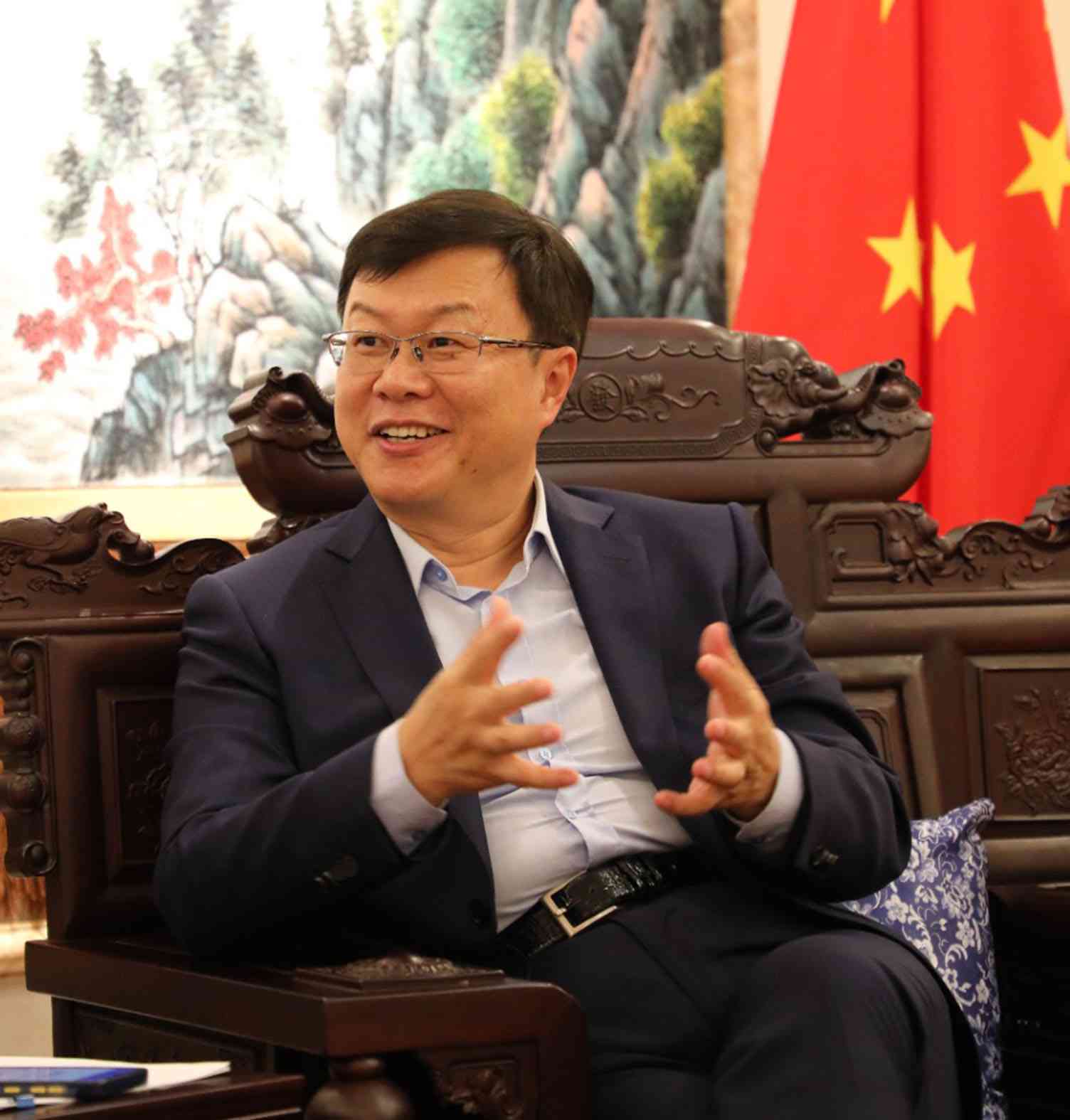

China writes off Zim debt deals

Zimbabwe currently owes a combined US$17,5 billion to foreign and local creditors.

By Tinashe Kairiza

Apr. 12, 2024

GMB owes wheat farmers US$35m

By Gamuchirai Nyamuziwa

Apr. 12, 2024

EU wants dialogue on investment climate

By Sydney Kawadza

Apr. 12, 2024

ExecutiveChat: ‘Have been in banking all my life’

Local News

By Faith Zaba | Apr. 12, 2024

ExecutiveChat: ‘Have been in banking all my life’

So what were your major highlights during your tenure as CEO of FBC?

By Faith Zaba

Apr. 12, 2024

Mushayavanhu refutes FBC shareholding claims

By Freeman Makopa

Apr. 12, 2024

GMB owes wheat farmers US$35m

By Gamuchirai Nyamuziwa

Apr. 12, 2024

Authorities rally behind ZiG

By Blessed Ndlovu and Belinda Chiroodza

Apr. 12, 2024

Rest, good sleep contribute to better health, happiness

By Admin

Feb. 17, 2023

Everyone eligible is encouraged to donate blood, help save lives

By The Independent

Jun. 10, 2022

2024 monetary policy: Review and analysis

By Zvikomborero Sibanda

Apr. 12, 2024

MPS, outlook conference resolutions

By Batanai Matsika

Apr. 12, 2024

Benefits, concerns of illegal artisanal gold mining in Zim

By Gloria Ndoro-mkombachoto

Apr. 12, 2024

Walking the sustainability talk

By Cynthia Tapera

Apr. 12, 2024

Hope for lifting ban on OM, PPC chips

By The Independent

Aug. 26, 2022

Without planes, AirZim board won’t perform wonders

By The Independent

Aug. 5, 2022

Power crisis needs urgent attention

By The Independent

Jul. 29, 2022

Don’t print cash for projects

By The Independent

Jul. 22, 2022

By NewsDay

Mar. 1, 2024

By NewsDay

Mar. 1, 2024

By NewsDay

Oct. 26, 2023

By NewsDay

Oct. 24, 2023

By NewsDay

Oct. 19, 2023

By NewsDay

Oct. 19, 2023

By NewsDay

Oct. 4, 2023

By NewsDay

Oct. 3, 2023

By NewsDay

Oct. 3, 2023

By NewsDay

Sep. 5, 2023

By NewsDay

Aug. 30, 2023

By NewsDay

Aug. 26, 2023

Exploring the vibrant world of sports betting in Ethiopia

While the allure of sports betting is undeniable, it's crucial to approach it with caution and responsibility.

By Theindependent

Mar. 11, 2024

Satewave churns out power solutions for Zim

Satewave Technologies director Xiao Feng said the company has several solar solutions to address the current power challenges.

By Staff Writer

Aug. 15, 2023

Liquid Tech to increase tariffs by 50%

By Staff Writer

Mar. 31, 2023

Jotter: Students develop an integrated learning app

By Staff Writer

Mar. 17, 2023

Innovative crowd-investing app ‘PiggyBankAdvisor’ launched

By Staff Writer

Mar. 17, 2023

Meta gives up on NFTs for Facebook and Instagram

By The Verge

Mar. 15, 2023

Reasons To Buy Bitcoin From A Trading Platform

Another fundamental reason behind getting the coins from this particular space is that it provides

By Theindependent

Mar. 2, 2023

Why do banks not want people to rely upon cryptocurrencies?

Cryptocurrency transaction volume is much less than the fiat currencies, leading to a lack of liquidity in the market.

By Theindependent

Feb. 9, 2023

Warriors back in Afcon draw

Mapeza is likely to preside over the next set of matches after he was roped in as an interim coach last month.

By Kevin Mapasure

Apr. 12, 2024

Book Review: African decolonisation in Southern Rhodesian Politics, 1950–1963

By Anotida Chikumbu

Apr. 12, 2024

Moozy captivates audience at homecoming showcase

By Khumbulani Muleya

Apr. 12, 2024

Women take over the stage at Sofar

Cites that hosted Sofar shows on the same day included Taipei (Taiwan), Riga (Latvia), Toulouse (France) and Quito in Ecuador.

By Staff Writer

Mar. 28, 2024

Japanese pop culture comes to life in Harare

By Khumbulani Muleya

Mar. 22, 2024

Fawezi wraps up GBV prevention initiative

By Khumbulani Muleya

Mar. 15, 2024

New children’s book a magical adventure

By Khumbulani Muleya

Mar. 15, 2024

Herbicides: Bad news for local food security

By The Independent

May. 27, 2022

Dumpsite: Gweru feels the heat

By The Independent

May. 13, 2022

Zim to pay 100% of international hunting revenue to communities

By The Independent

Jun. 10, 2022

.

Videos

Pamela Marwisa In Conversation With Trevor

By The NewsDay

Feb. 28, 2024

Job Sikhala, Zimbabwean Opposition Politician In Conversation With Trevor

By The NewsDay

Feb. 28, 2024

ExtremeWeather: Parts of Harare experienced flash floods on Sunday

By The NewsDay

Dec. 21, 2023

Harare motorists negotiate the city’s treacherous roads

By The NewsDay

Dec. 21, 2023

Solomon Guramatunhu Day 1

By The NewsDay

Dec. 14, 2023

Sengezo Tshabangu - In Conversation With Trevor

By The NewsDay

Dec. 5, 2023

Welcome to Alpha Media Holdings Zimbabwe - NewsDay - The Standard - The Zim Independent

By The NewsDay

Dec. 5, 2023

Dock sheep tail to maintain weight

The most common way of docking tails is by using an elastic and expandable latex ring. The rubber ring is expanded with an elastrator and put over the tail, where it is released.

By Kudakwashe Gwabanayi

Mar. 22, 2024

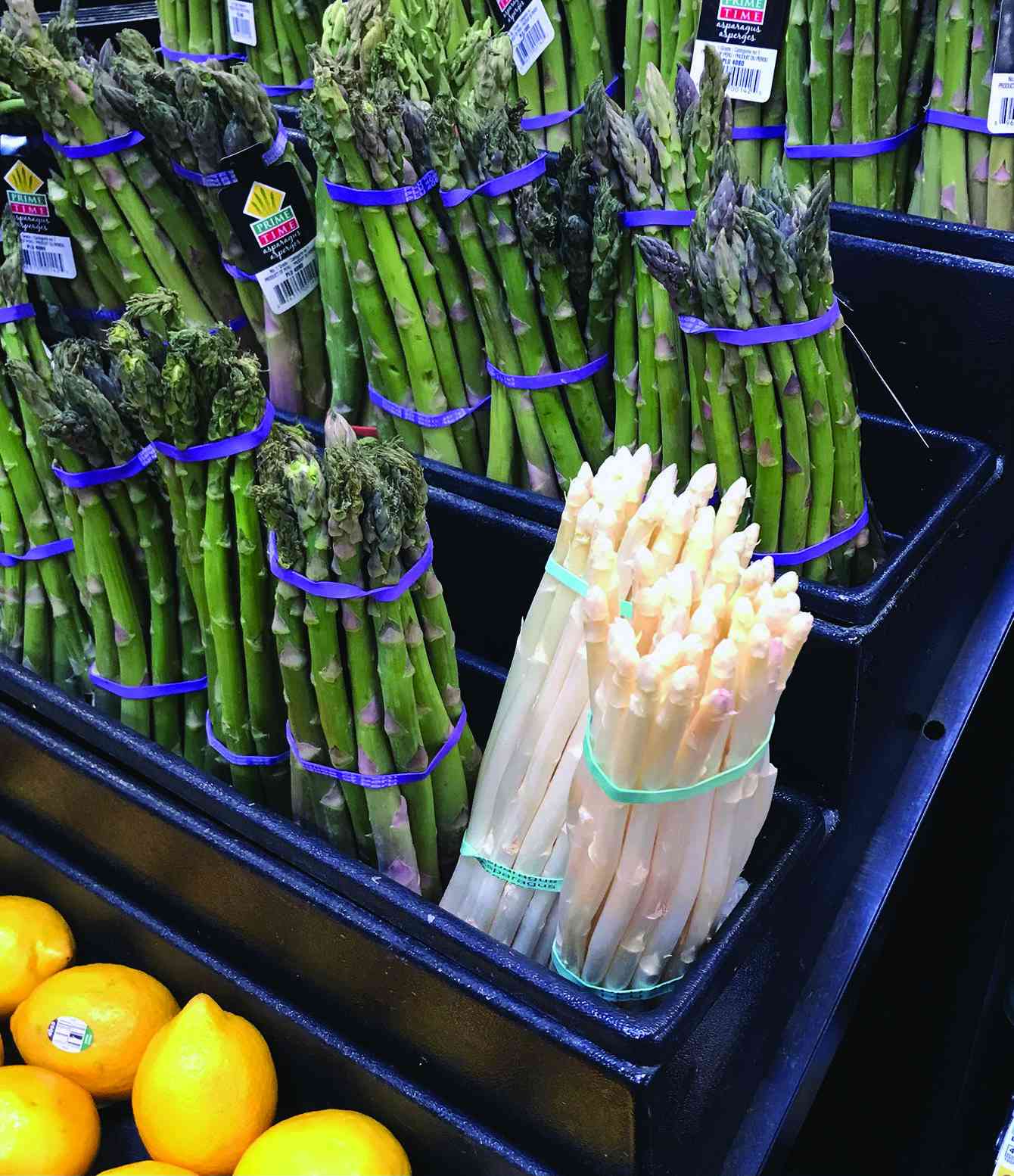

Asparagus worth your while (II)

By Kudakwashe Gwabanayi

Mar. 1, 2024

Why it makes sense to farm meat goats

By Shane Brody

Jul. 7, 2023

How to start a fish farming business

By Kudakwashe Gwabanayi

May. 26, 2023

Climate change is real, be alert

By Kudakwashe Gwabanayi

May. 12, 2023

EdutainmentMix: Glamour, grit, and grace: A model’s guide to self confidence

Nowadays every person who owns a smart phone can take a picture and in the process pose as a model.

By Raymond Millagre Langa

Apr. 14, 2024

InnBucks pours US$5 million into operations

InnBucks has determined the functional currency as the United States dollar.

By Tatira Zwinoira

Apr. 14, 2024

RBZ snubs forex auction bidders

By Melody Chikono

Apr. 14, 2024

GhettoDances: Gossip only breeds confusion and enmity

By Onie Ndoro

Apr. 14, 2024

Govt invests US$13m in early warning systems

By Melody Chikono

Apr. 14, 2024

Out & About: The hum incubating Kehlani’s scales

By Grant Moyo

Apr. 14, 2024

BCC rakes in thousands in fines

The local authority also noted that open air worshippers were on the increase both in the eastern and western suburbs.

By Silas Nkala

6h ago

CCC Bulawayo meets after Chamisa’s departure

The other co-president, Tendai Biti, has since quit opposition politics under unclear circumstances saying he intended to take a sabbatical.

By Nizbert Moyo

6h ago

Byo housing scammer nabbed

By Nizbert Moyo

Apr. 15, 2024

Pumula residents, Chinese miner clash over noise

By Innocent Magondo and Patricia Sibanda

Apr. 15, 2024

Zebra meat lands Binga man in trouble

By Daniel Moyo

Apr. 15, 2024

Independent but not free; use of the law to silence critics in Zimbabwe-the true story of our independence

Through the passing of legislation making opposition mobilization more difficult, the government became increasingly isolated.

By Mlondolozi Ndlovu

2h ago

GET OUR NEWSLETTER

Subscribe to our newsletter and stay updated on the latest developments and special offers!

SUBSCRIBECONNECT WITH US

SUPPORT INDEPENDENT JOURNALISM